What Investors Need to Know Ahead of Big Canadian Bank Earnings Reports

The fiscal Q3 earnings for the Canadian Big Five Banks are forecast to show an overall modest increase in earnings per share of approximately 5%, which could be offset by a downturn for Scotiabank due to higher loan-loss provisions. Revenue is projected to increase by an average of 4%, despite tepid loan growth, buoyed by a stable net interest margin. The strong presence in capital markets may prove advantageous for certain banks, with RBC positioned to benefit from increased fee revenue.

In a recent August report, Fitch Ratings offered insights into Canadian banks, forecasting that the nation's largest financial institutions are likely to experience "modest earnings growth" amid a subdued economic landscape in 2024 and 2025. Among these banks, the Royal Bank of Canada (RBC) is predicted to outperform its competitors. Maria Gabriella Khoury, Fitch Ratings' senior director, stated, "The stabilization of Canada's economy is expected to bolster the financial results of banks in the latter half of 2024." She further noted, "Canadian banks generally maintain a conservative risk profile, bolstered by well-controlled exposure and prudent underwriting practices, which have historically resulted in low levels of loan impairments and credit losses."

The earnings reports are scheduled to begin with TD on August 22, followed by Scotiabank and BMO on August 27, RBC on August 28, and CIBC concluding the sequence on August 29, respectively.

Here are the key points that investors need to focus on:

Revenue Gains May Vary; Provisions Rise

The five largest Canadian banks may report a wider-than-usual range of fiscal Q3 results, with a consensus projecting a 4% rise in revenue and individual estimates ranging from -0.2% to 6%, driven by fees and capital-market operations. The projected earnings increase averages 5%, but estimates vary widely, from a decrease of 6% to an increase of 14%, as loan-loss provisions may differ significantly, with an average increase of 40%.

RBC and BMO are poised to see benefits from synergies related to recent acquisitions, whereas Scotiabank's latest banking deals might prompt further queries. Loan volume is likely to grow by a modest low-to-mid single-digit percentage, and net interest income could experience limited growth despite potentially stable margins. Effective cost management strategies may lead to improved operating leverage.

Yield-Curve Inversion Moves With Rate-Cuts Outlook, Easing Funding Costs Pressure

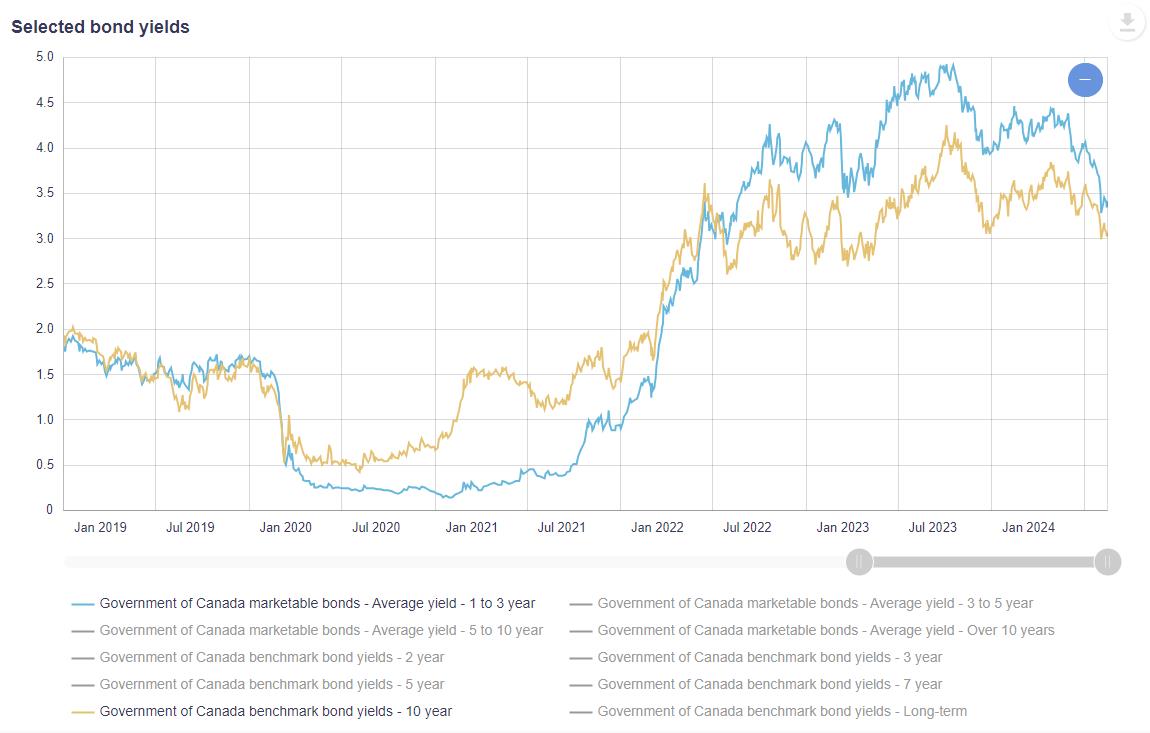

Net interest income is a critical component of a bank's profitability. In a typical economic climate, banks enjoy the benefits of a positive yield curve, characterized by higher interest rates on loans with extended maturities compared to the lower rates on short-term liabilities. This dynamic enables banks to borrow funds at lower costs in the short run and extend credit at higher rates over the long run, leading to a significant net interest margin.

However, this margin faces compression when the yield difference between short-term and long-term debt, such as one-year and ten-year yields, decreases or reverses. An inverted yield curve, where long-term rates fall below short-term rates, can squeeze the net interest margin.

Canada's yield curve remains inverted, with long rates below those in fiscal Q2. The Bank of Canada has cut rates twice, with the potential for more this year. Market pricing implies about 50 bps of cumulative rate cuts before the year-end, though some still anticipate more. The yield spread between one-year and ten-year bonds, at negative 84 bps by July's end, has compressed by 14 bps from the prior month and is 12 bps less than it was in April. This shows an easing in the pressure from funding costs on net interest margins.

Toronto-Dominion, CIBC, and Scotiabank depend the most on interest income, whereas the Royal Bank of Canada and the Bank of Montreal rely more on fees. CIBC stands out for having the most considerable exposure to the Canadian market.

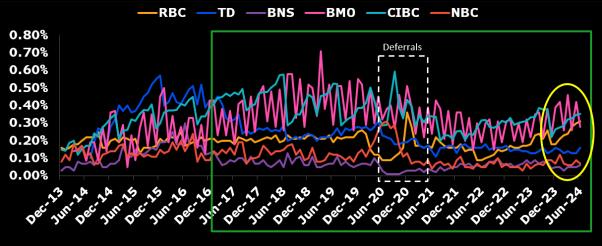

Mortgage Delinquencies Slightly Increase

In June, Canadian banks saw a slight increase in serious mortgage delinquencies within their covered-bond pools, with a rise of 2 bps compared to the previous year. Late payments on borrowings under 90 days experienced a modest increase, particularly for RBC and BMO, though these numbers remain below the levels seen in March 2020 for all banks. For loans delinquent by 90 days or more, BMO and RBC observed a 4 bps increase, National Bank and CIBC a 1 bp rise (notably, CIBC had added new loans in November), while the rates at TD and Scotiabank remained relatively stable. The credit quality for these covered-bond pools has been gradually declining, with ongoing risks from higher interest rates despite the Bank of Canada's rate cuts in June.

Overall, delinquency rates were 4 bps higher in June than in the same month last year and had risen by 2 bps in the first half of the year. The initial impact of this pressure was most pronounced among borrowers with lower-quality and variable-rate loans.

Credit Card Delinquency Rates Climb

Rising debt levels and high interest rates are leading to an increase in credit card delinquency rates at Canada's major banks, and this trend may continue despite a temporary decrease noted in May. BMO reported the most significant rise, with delinquency rates reaching 75 bps, followed by RBC at 43 bps, and TD at 25 bps. Conversely, CIBC saw some relief due to the expansion of its credit pool. June experienced a 29 bps jump in late payments compared to the same month last year, with delinquencies of 90 days or more standing 14 bps higher year-over-year, indicative of significant consumer financial stress. These figures, which can vary depending on the loan types included in the trusts, are from the card-trust portfolios of Golden Credit Card Trust (RBC), Evergreen Credit Card Trust (TD), Trillium Credit Card Trust II (Scotiabank), Master Credit Card Trust (BMO), and CARDS II Trust (CIBC).

Capital Adequacy Remains Stable

The capital adequacy ratios for the major banks are anticipated to stay stable and well above regulatory requirements. TD is the only one among the big five to see a decrease in its capital adequacy ratio from the previous quarter, yet it continues to maintain the highest ratio among its peers. TD's Common Equity Tier 1 (CET1) ratio stood at 13.40% at the end of Q2, and provisions for AML investigations and civil matters are expected to impact it by 13 bps in Q3.

Investors who focus on Canadian banks can also keep an eye on bank ETFs.

$BMO EQUAL WEIGHT BANKS INDEX ETF TRUST UNIT (ZEB.CA)$ has net assets of approximately CAD 3.88 billion and a management fee of 0.28%. Its largest holding is RBC, accounting for about 18.5% of the fund's assets.

Another option is the $BMO COVERED CALL CANADIAN BANKS ETF UNIT (ZWB.CA)$. Due to the use of call options, the fund currently has an annualized dividend yield of 7.24%, but it also has a higher management fee (0.65%).

The $ISHARES CDN FINANCIAL MTHLY INC FD COM UNIT (FIE.CA)$ is a diversified allocation ETF. Specifically, approximately 37% of the ETF's funds are allocated to Canada's six largest bank stocks, 19% to the preferred stocks of the iShares S&P/TSX Canadian Preferred Share Index ETF, and 10% to corporate bonds of the iShares Core Canadian Corporate Bond Index ETF.

Source: Bloomberg, Yahoo Finance Canada

$The Toronto-Dominion Bank (TD.US)$ $The Toronto-Dominion Bank (TD.CA)$ $Royal Bank of Canada (RY.CA)$ $Royal Bank of Canada (RY.US)$ $Bank of Montreal (BMO.CA)$ $Bank of Montreal (BMO.US)$ $Bank of Nova Scotia (BNS.CA)$ $Bank of Nova Scotia (BNS.CA)$ $Canadian Imperial Bank of Commerce (CM.US)$ $Canadian Imperial Bank of Commerce (CM.CA)$

Disclaimer: Moomoo Technologies Inc. is providing this content for information and educational use only.

Read more

Comment

Sign in to post a comment

Moomoo news official account

Follow the top news of Canadian market!

1239Followers

5Following

3135Visitors

Follow