Time To Worry? Analysts Are Downgrading Their Huafon Chemical Co., Ltd. (SZSE:002064) Outlook

Time To Worry? Analysts Are Downgrading Their Huafon Chemical Co., Ltd. (SZSE:002064) Outlook

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. We would highlight that sales are expected to reverse, with a forecast 30% annualised revenue decline to the end of 2023. That is a notable change from historical growth of 17% over the last five years. Compare this with our data, which suggests that other companies in the same industry are, in aggregate, expected to see their revenue grow 19% per year. It's pretty clear that Huafon Chemical's revenues are expected to perform substantially worse than the wider industry.

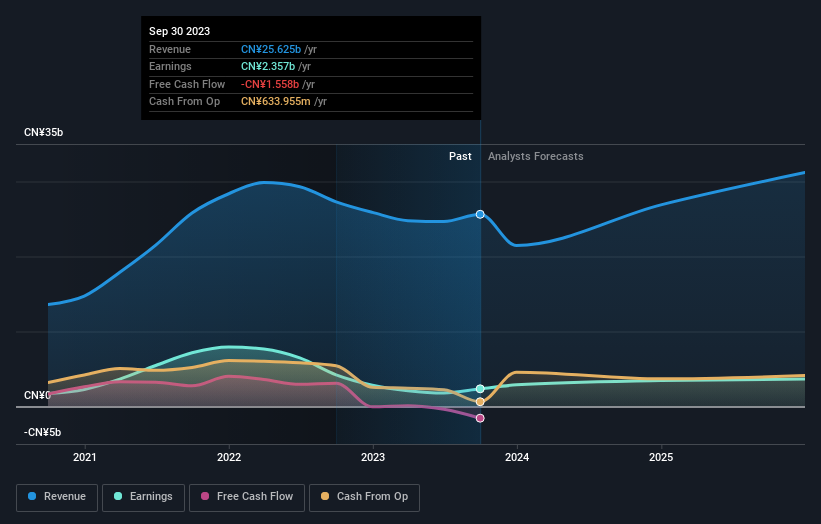

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. We would highlight that sales are expected to reverse, with a forecast 30% annualised revenue decline to the end of 2023. That is a notable change from historical growth of 17% over the last five years. Compare this with our data, which suggests that other companies in the same industry are, in aggregate, expected to see their revenue grow 19% per year. It's pretty clear that Huafon Chemical's revenues are expected to perform substantially worse than the wider industry. The analysts covering Huafon Chemical Co., Ltd. (SZSE:002064) delivered a dose of negativity to shareholders today, by making a substantial revision to their statutory forecasts for this year. Both revenue and earnings per share (EPS) estimates were cut sharply as the analysts factored in the latest outlook for the business, concluding that they were too optimistic previously. The stock price has risen 4.5% to CN¥7.21 over the past week. We'd be curious to see if the downgrade is enough to reverse investor sentiment on the business.

覆盖的分析师华丰化工股份有限公司深圳证券交易所(SZSE:002064)今天对股东今年的法定预测进行了大幅修订,给股东们带来了一些负面影响。营收和每股收益(EPS)预期均大幅下调,因为分析师将最新的业务前景考虑在内,得出结论认为他们之前过于乐观。过去一周,该公司股价上涨4.5%,至7.21元。我们很想知道,评级下调是否足以扭转投资者对该业务的情绪。

Following the downgrade, the consensus from three analysts covering Huafon Chemical is for revenues of CN¥21b in 2023, implying an uneasy 16% decline in sales compared to the last 12 months. Per-share earnings are expected to swell 19% to CN¥0.56. Previously, the analysts had been modelling revenues of CN¥24b and earnings per share (EPS) of CN¥0.63 in 2023. It looks like analyst sentiment has declined substantially, with a substantial drop in revenue estimates and a real cut to earnings per share numbers as well.

评级下调后,研究华丰化工的三位分析师的共识是,2023年的收入将达到人民币210亿元,这意味着与过去12个月相比,销售额将下降16%,这令人感到不安。每股收益预计将增长19%,至0.56加元。此前,分析师一直在预测2023年的收入为人民币240亿元,每股收益为人民币0.63元。看起来分析师的情绪已经大幅下降,营收预期大幅下降,每股收益数字也大幅下降。

Check out our latest analysis for Huafon Chemical

查看我们对华丰化工的最新分析

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. We would highlight that sales are expected to reverse, with a forecast 30% annualised revenue decline to the end of 2023. That is a notable change from historical growth of 17% over the last five years. Compare this with our data, which suggests that other companies in the same industry are, in aggregate, expected to see their revenue grow 19% per year. It's pretty clear that Huafon Chemical's revenues are expected to perform substantially worse than the wider industry.

现在看一看更大的图景,我们可以理解这些预测的方法之一是看看它们与过去的业绩和行业增长估计如何比较。我们要强调的是,销售预计将逆转,预计到2023年底,年化收入将下降30%。与过去五年17%的历史增长率相比,这是一个显著的变化。与我们的数据相比,我们的数据表明,同一行业的其他公司预计收入将以每年19%的速度增长。很明显,华丰化工的营收预计将远远逊于整个行业。

The Bottom Line

底线

The most important thing to take away is that analysts cut their earnings per share estimates, expecting a clear decline in business conditions. Unfortunately analysts also downgraded their revenue estimates, and industry data suggests that Huafon Chemical's revenues are expected to grow slower than the wider market. After a cut like that, investors could be forgiven for thinking analysts are a lot more bearish on Huafon Chemical, and a few readers might choose to steer clear of the stock.

最重要的是,分析师们下调了每股收益预期,预计商业环境将出现明显下滑。不幸的是,分析师也下调了他们的营收预期,行业数据显示,华丰化工的营收增速预计将低于大盘。在这样的下跌之后,投资者认为分析师对华丰化学的看法要悲观得多,这是情有可原的,一些读者可能会选择避开该股。

There might be good reason for analyst bearishness towards Huafon Chemical, like concerns around earnings quality. For more information, you can click here to discover this and the 2 other concerns we've identified.

分析师看空华丰化工或许是有充分理由的,比如对盈利质量的担忧。有关更多信息,您可以单击此处了解这一点以及我们确定的其他两个问题。

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

搜索有趣的公司的另一种方式可能是到达拐点是跟踪管理层是在买入还是在卖出,我们的免费内部人士正在收购的成长型公司名单。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

对这篇文章有什么反馈吗?担心内容吗? 保持联系直接与我们联系。或者,也可以给编辑组发电子邮件,地址是implywallst.com。

本文由Simply Wall St.撰写,具有概括性。我们仅使用不偏不倚的方法提供基于历史数据和分析师预测的评论,我们的文章并不打算作为财务建议。它不构成买卖任何股票的建议,也没有考虑你的目标或你的财务状况。我们的目标是为您带来由基本面数据驱动的长期重点分析。请注意,我们的分析可能不会将最新的对价格敏感的公司公告或定性材料考虑在内。Simply Wall St.对上述任何一只股票都没有持仓。