Natural Gas Services Group, Inc. (NYSE:NGS) Stocks Shoot Up 29% But Its P/S Still Looks Reasonable

Natural Gas Services Group, Inc. (NYSE:NGS) Stocks Shoot Up 29% But Its P/S Still Looks Reasonable

Despite an already strong run, Natural Gas Services Group, Inc. (NYSE:NGS) shares have been powering on, with a gain of 29% in the last thirty days. The last 30 days bring the annual gain to a very sharp 43%.

儘管已經表現強勁,天然氣服務集團公司(紐約證券交易所代碼:NGS)的股票一直在上漲,在過去的30天裡上漲了29%。在過去的30天裡,年度漲幅達到了非常大的43%。

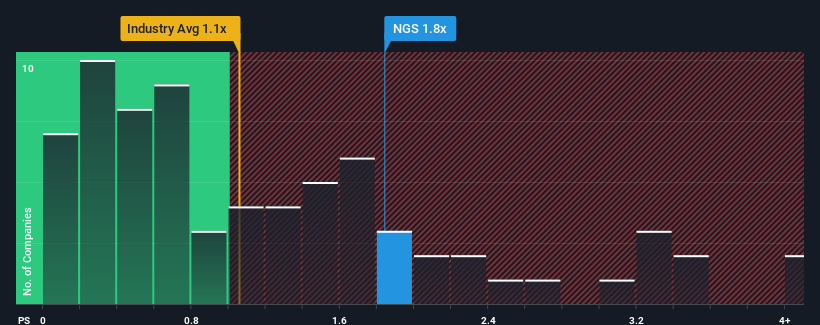

After such a large jump in price, you could be forgiven for thinking Natural Gas Services Group is a stock not worth researching with a price-to-sales ratios (or "P/S") of 1.8x, considering almost half the companies in the United States' Energy Services industry have P/S ratios below 1.1x. However, the P/S might be high for a reason and it requires further investigation to determine if it's justified.

在價格如此大幅上漲後,你可能會認為天然氣服務集團是一隻不值得研究的股票,市銷率(P/S)為1.8倍,考慮到美國能源服務行業近一半的公司的本益比/S比率低於1.1倍,你也可以理解。然而,P/S可能是有原因的,需要進一步調查才能確定是否合理。

View our latest analysis for Natural Gas Services Group

查看我們對天然氣服務集團的最新分析

What Does Natural Gas Services Group's Recent Performance Look Like?

天然氣服務集團近期的表現如何?

Recent revenue growth for Natural Gas Services Group has been in line with the industry. It might be that many expect the mediocre revenue performance to strengthen positively, which has kept the P/S ratio from falling. However, if this isn't the case, investors might get caught out paying too much for the stock.

天然氣服務集團最近的收入增長與行業一致。這可能是因為許多人預計平庸的營收表現將積極增強,這使得本益比/S比率沒有下降。然而,如果情況並非如此,投資者可能會被髮現為該股支付過高的價格。

What Are Revenue Growth Metrics Telling Us About The High P/S?

收入增長指標告訴我們關於高本益比的哪些資訊?

There's an inherent assumption that a company should outperform the industry for P/S ratios like Natural Gas Services Group's to be considered reasonable.

有一個固有的假設,即一家公司的表現應該優於行業,才能讓天然氣服務集團這樣的本益比被認為是合理的。

If we review the last year of revenue growth, the company posted a terrific increase of 28%. The latest three year period has also seen a 29% overall rise in revenue, aided extensively by its short-term performance. Therefore, it's fair to say the revenue growth recently has been respectable for the company.

如果我們回顧過去一年的收入增長,該公司公佈了28%的驚人增長。在最近三年中,該公司的整體收入增長了29%,這在很大程度上得益於其短期表現。因此,公平地說,最近的收入增長對公司來說是值得尊敬的。

Turning to the outlook, the next year should generate growth of 24% as estimated by the two analysts watching the company. With the industry only predicted to deliver 14%, the company is positioned for a stronger revenue result.

談到前景,正如兩位關注該公司的分析師估計的那樣,明年應該會產生24%的增長。由於該行業預計將僅貢獻14%的收入,該公司將迎來更強勁的收入結果。

With this information, we can see why Natural Gas Services Group is trading at such a high P/S compared to the industry. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

有了這個資訊,我們就可以理解為什麼天然氣服務集團的本益比比行業高出這麼高的S。顯然,股東們並不熱衷於出售那些可能著眼於更繁榮未來的資產。

The Final Word

最後的結論

Natural Gas Services Group shares have taken a big step in a northerly direction, but its P/S is elevated as a result. Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

天然氣服務集團(Natural Gas Services Group)的股票向北邁出了一大步,但其本益比(P/S)因此上升。僅僅用市銷率來決定你是否應該出售你的股票是不明智的,但它可以成為公司未來前景的實用指南。

As we suspected, our examination of Natural Gas Services Group's analyst forecasts revealed that its superior revenue outlook is contributing to its high P/S. At this stage investors feel the potential for a deterioration in revenues is quite remote, justifying the elevated P/S ratio. Unless the analysts have really missed the mark, these strong revenue forecasts should keep the share price buoyant.

正如我們所懷疑的那樣,我們對天然氣服務集團分析師預測的審查顯示,其優越的收入前景是導致其高本益比的原因之一。在此階段,投資者認為收入惡化的可能性微乎其微,證明瞭較高的P/S比率是合理的。除非分析師們真的沒有達到預期,否則這些強勁的收入預測應該會讓股價保持上漲。

Having said that, be aware Natural Gas Services Group is showing 2 warning signs in our investment analysis, and 1 of those is a bit concerning.

話雖如此,但請注意天然氣服務集團出現兩個警示信號在我們的投資分析中,其中一項有點令人擔憂。

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

重要的是確保你尋找的是一家偉大的公司,而不僅僅是你遇到的第一個想法。因此,如果不斷增長的盈利能力符合你對一家偉大公司的看法,不妨看看這一點免費近期收益增長強勁(本益比較低)的有趣公司名單。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

對這篇文章有什麼反饋嗎?擔心內容嗎? 保持聯繫直接與我們聯繫.或者,也可以給編輯組發電子郵件,地址是暗示Wallst.com。

本文由Simply Wall St.撰寫,具有概括性.我們僅使用不偏不倚的方法提供基於歷史數據和分析師預測的評論,我們的文章並不打算作為財務建議.它不構成買賣任何股票的建議,也沒有考慮你的目標或你的財務狀況.我們的目標是為您帶來由基本面數據驅動的長期重點分析.請注意,我們的分析可能不會將最新的對價格敏感的公司公告或定性材料考慮在內.Simply Wall St.對上述任何一隻股票都沒有持倉.