Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that Royal Caribbean Cruises Ltd. (NYSE:RCL) does use debt in its business. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

What Is Royal Caribbean Cruises's Net Debt?

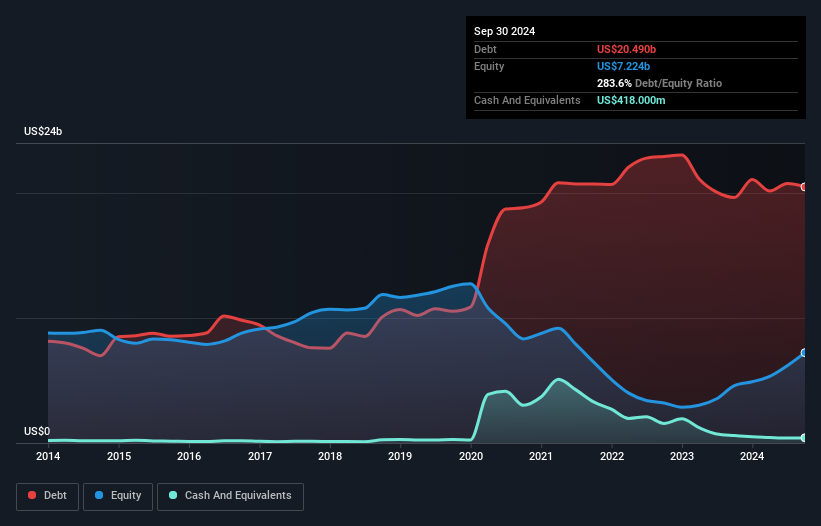

As you can see below, at the end of September 2024, Royal Caribbean Cruises had US$20.5b of debt, up from US$19.6b a year ago. Click the image for more detail. On the flip side, it has US$418.0m in cash leading to net debt of about US$20.1b.

NYSE:RCL Debt to Equity History December 24th 2024

How Strong Is Royal Caribbean Cruises' Balance Sheet?

The latest balance sheet data shows that Royal Caribbean Cruises had liabilities of US$9.63b due within a year, and liabilities of US$20.2b falling due after that. On the other hand, it had cash of US$418.0m and US$441.0m worth of receivables due within a year. So it has liabilities totalling US$29.0b more than its cash and near-term receivables, combined.

Royal Caribbean Cruises has a very large market capitalization of US$64.1b, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

While we wouldn't worry about Royal Caribbean Cruises's net debt to EBITDA ratio of 3.6, we think its super-low interest cover of 2.5 times is a sign of high leverage. So shareholders should probably be aware that interest expenses appear to have really impacted the business lately. Looking on the bright side, Royal Caribbean Cruises boosted its EBIT by a silky 76% in the last year. Like a mother's loving embrace of a newborn that sort of growth builds resilience, putting the company in a stronger position to manage its debt. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Royal Caribbean Cruises's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So we always check how much of that EBIT is translated into free cash flow. Looking at the most recent two years, Royal Caribbean Cruises recorded free cash flow of 32% of its EBIT, which is weaker than we'd expect. That's not great, when it comes to paying down debt.

Our View

On our analysis Royal Caribbean Cruises's EBIT growth rate should signal that it won't have too much trouble with its debt. However, our other observations weren't so heartening. To be specific, it seems about as good at covering its interest expense with its EBIT as wet socks are at keeping your feet warm. When we consider all the factors mentioned above, we do feel a bit cautious about Royal Caribbean Cruises's use of debt. While debt does have its upside in higher potential returns, we think shareholders should definitely consider how debt levels might make the stock more risky. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. For example, we've discovered 3 warning signs for Royal Caribbean Cruises (1 is concerning!) that you should be aware of before investing here.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

オーストラリアでは、moomooの投資商品及びサービスはMoomoo Securities Australia Limitedによって提供され、オーストラリア証券投資委員会(ASIC)の管理を受けております(AFSL No. 224663)。「金融サービスガイド」、「利用規約」、「プライバシーポリシー」などの詳細は、Moomoo Securities Australia Limitedのウェブサイトhttps://www.moomoo.com/auでご確認いただけます。

オーストラリアでは、moomooの投資商品及びサービスはMoomoo Securities Australia Limitedによって提供され、オーストラリア証券投資委員会(ASIC)の管理を受けております(AFSL No. 224663)。「金融サービスガイド」、「利用規約」、「プライバシーポリシー」などの詳細は、Moomoo Securities Australia Limitedのウェブサイトhttps://www.moomoo.com/auでご確認いただけます。

The latest balance sheet data shows that Royal Caribbean Cruises had liabilities of US$9.63b due within a year, and liabilities of US$20.2b falling due after that. On the other hand, it had cash of US$418.0m and US$441.0m worth of receivables due within a year. So it has liabilities totalling US$29.0b more than its cash and near-term receivables, combined.

The latest balance sheet data shows that Royal Caribbean Cruises had liabilities of US$9.63b due within a year, and liabilities of US$20.2b falling due after that. On the other hand, it had cash of US$418.0m and US$441.0m worth of receivables due within a year. So it has liabilities totalling US$29.0b more than its cash and near-term receivables, combined.

ロイヤル・カリビアン・クルーズは非常に大きな時価総額641億米ドルを持っているため、必要が生じた場合にはバランスシートを改善するために現金を調達することが非常に可能性が高い。しかし、確実にその負債がリスクを過度にもたらしている兆候には注意を払いたい。

ロイヤル・カリビアン・クルーズは非常に大きな時価総額641億米ドルを持っているため、必要が生じた場合にはバランスシートを改善するために現金を調達することが非常に可能性が高い。しかし、確実にその負債がリスクを過度にもたらしている兆候には注意を払いたい。