Singapore Airlines Limited's (SGX:C6L) Stock Is Rallying But Financials Look Ambiguous: Will The Momentum Continue?

Singapore Airlines Limited's (SGX:C6L) Stock Is Rallying But Financials Look Ambiguous: Will The Momentum Continue?

Singapore Airlines' (SGX:C6L) stock is up by a considerable 19% over the past three months. However, we wonder if the company's inconsistent financials would have any adverse impact on the current share price momentum. Particularly, we will be paying attention to Singapore Airlines' ROE today.

新加坡航空(SGX: C6L)的股票在过去三个月中大幅上涨了19%。但是,我们想知道该公司不一致的财务状况是否会对当前的股价势头产生任何不利影响。特别是,我们今天将关注新加坡航空的投资回报率。

ROE or return on equity is a useful tool to assess how effectively a company can generate returns on the investment it received from its shareholders. Put another way, it reveals the company's success at turning shareholder investments into profits.

投资回报率或股本回报率是评估公司如何有效地从股东那里获得投资回报的有用工具。换句话说,它揭示了公司成功地将股东投资转化为利润。

Check out our latest analysis for Singapore Airlines

查看我们对新加坡航空的最新分析

How Do You Calculate Return On Equity?

你如何计算股本回报率?

The formula for ROE is:

这个 投资回报率公式 是:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

股本回报率 = 净利润(来自持续经营)≥ 股东权益

So, based on the above formula, the ROE for Singapore Airlines is:

因此,根据上述公式,新加坡航空的投资回报率为:

11% = S$2.2b ÷ S$20b (Based on the trailing twelve months to March 2023).

11% = 22亿新元 ÷ 200亿新元(基于截至2023年3月的过去十二个月)。

The 'return' is the profit over the last twelve months. That means that for every SGD1 worth of shareholders' equity, the company generated SGD0.11 in profit.

“回报” 是过去十二个月的利润。这意味着,公司每获得价值1新加坡元的股东权益,就会产生0.11新加坡元的利润。

What Has ROE Got To Do With Earnings Growth?

投资回报率与收益增长有什么关系?

Thus far, we have learned that ROE measures how efficiently a company is generating its profits. We now need to evaluate how much profit the company reinvests or "retains" for future growth which then gives us an idea about the growth potential of the company. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don't share these attributes.

到目前为止,我们已经了解到,投资回报率衡量的是公司创造利润的效率。现在,我们需要评估公司再投资或 “保留” 了多少利润以用于未来的增长,从而使我们对公司的增长潜力有所了解。一般而言,在其他条件相同的情况下,股本回报率和利润留存率高的公司的增长率要高于不具有这些属性的公司。

Singapore Airlines' Earnings Growth And 11% ROE

新加坡航空的收益增长和11%的投资回报率

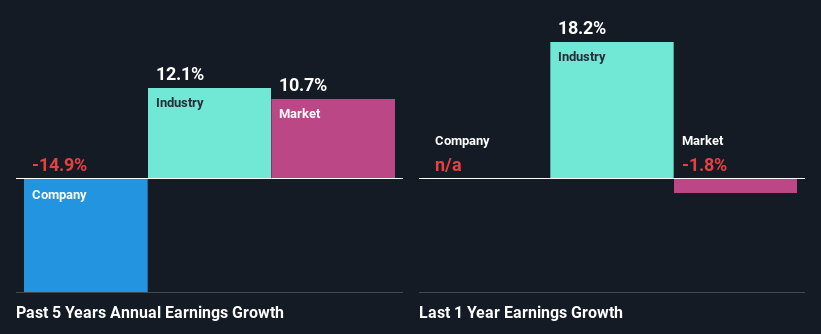

At first glance, Singapore Airlines seems to have a decent ROE. Further, the company's ROE is similar to the industry average of 13%. However, while Singapore Airlines has a pretty respectable ROE, its five year net income decline rate was 15% . We reckon that there could be some other factors at play here that are preventing the company's growth. For example, it could be that the company has a high payout ratio or the business has allocated capital poorly, for instance.

乍一看,新加坡航空的投资回报率似乎不错。此外,该公司的投资回报率与行业平均水平的13%相似。但是,尽管新加坡航空的投资回报率相当可观,但其五年净收入下降率为15%。我们认为,这里可能还有其他一些因素在起作用,阻碍了公司的发展。例如,可能是公司的派息率很高,或者企业的资本配置不佳。

From the 15% decline reported by the industry in the same period, we infer that Singapore Airlines and its industry are both shrinking at a similar rate.

从同期该行业报告的15%下降中,我们推断出新加坡航空及其行业都在以相似的速度萎缩。

Earnings growth is an important metric to consider when valuing a stock. What investors need to determine next is if the expected earnings growth, or the lack of it, is already built into the share price. By doing so, they will have an idea if the stock is headed into clear blue waters or if swampy waters await. One good indicator of expected earnings growth is the P/E ratio which determines the price the market is willing to pay for a stock based on its earnings prospects. So, you may want to check if Singapore Airlines is trading on a high P/E or a low P/E, relative to its industry.

收益增长是估值股票时要考虑的重要指标。投资者接下来需要确定的是,预期的收益增长或缺乏收益增长是否已经包含在股价中。这样,他们就能知道这只种群是进入清澈的蓝色海水还是沼泽水域在等着你。预期收益增长的一个很好的指标是市盈率,市盈率根据收益前景决定了市场愿意为股票支付的价格。因此,您可能需要查看新加坡航空相对于其行业的市盈率是高还是低市盈率。

Is Singapore Airlines Making Efficient Use Of Its Profits?

新加坡航空是否在有效利用其利润?

Singapore Airlines' high LTM (or last twelve month) payout ratio of 107% suggests that the company is depleting its resources to keep up its dividend payments, and this shows in its shrinking earnings. Paying a dividend beyond their means is usually not viable over the long term. To know the 2 risks we have identified for Singapore Airlines visit our risks dashboard for free.

新加坡航空的LTM(或过去十二个月)派息率为107%,这表明该公司正在耗尽资源以维持股息支付,这体现在其收益的萎缩上。从长远来看,支付超出其承受能力的股息通常是不可行的。要了解我们为新加坡航空确定的两种风险,请免费访问我们的风险控制面板。

Moreover, Singapore Airlines has been paying dividends for at least ten years or more suggesting that management must have perceived that the shareholders prefer dividends over earnings growth. Existing analyst estimates suggest that the company's future payout ratio is expected to drop to 44% over the next three years. Regardless, the future ROE for Singapore Airlines is predicted to decline to 6.4% despite the anticipated decrease in the payout ratio. We reckon that there could probably be other factors that could be driving the forseen decline in the company's ROE.

此外,新加坡航空支付股息已经有至少十年或更长时间了,这表明管理层一定已经意识到股东更喜欢分红而不是收益增长。现有的分析师估计表明,该公司未来的派息率预计将在未来三年内降至44%。无论如何,尽管预计派息率会下降,但新加坡航空的未来投资回报率预计将降至6.4%。我们认为,可能还有其他因素可能推动公司投资回报率的预期下降。

Summary

摘要

In total, we're a bit ambivalent about Singapore Airlines' performance. While the company does have a high rate of return, its low earnings retention is probably what's hampering its earnings growth. Moreover, after studying current analyst estimates, we discovered that the company's earnings are expected to continue to shrink in the future. Are these analysts expectations based on the broad expectations for the industry, or on the company's fundamentals? Click here to be taken to our analyst's forecasts page for the company.

总的来说,我们对新加坡航空的表现有点矛盾。尽管该公司的回报率确实很高,但其低的收益保留率可能是阻碍其收益增长的原因。此外,在研究了当前分析师的估计之后,我们发现该公司的收益预计将在未来继续萎缩。这些分析师的预期是基于对该行业的广泛预期,还是基于公司的基本面?点击此处进入我们的分析师对公司的预测页面。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

对这篇文章有反馈吗?对内容感到担忧? 取得联系 直接和我们联系。 或者,给编辑团队 (at) simplywallst.com 发送电子邮件。

Simply Wall St 的这篇文章本质上是一般性的。 我们仅使用公正的方法提供基于历史数据和分析师预测的评论,我们的文章无意提供财务建议。 它不构成买入或卖出任何股票的建议,也没有考虑您的目标或财务状况。我们的目标是为您提供由基本面数据驱动的长期重点分析。请注意,我们的分析可能未将最新的价格敏感型公司公告或定性材料考虑在内。简而言之,华尔街对上述任何股票都没有头寸。