To the annoyance of some shareholders, Shanghai Guao Electronic Technology Co., Ltd. (SZSE:300551) shares are down a considerable 38% in the last month, which continues a horrid run for the company. The drop over the last 30 days has capped off a tough year for shareholders, with the share price down 42% in that time.

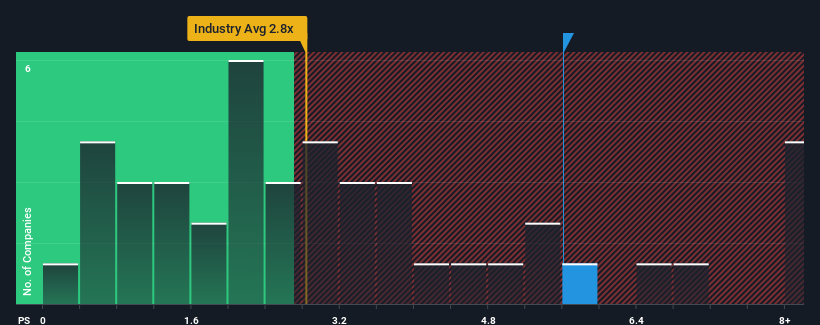

In spite of the heavy fall in price, you could still be forgiven for thinking Shanghai Guao Electronic Technology is a stock to steer clear of with a price-to-sales ratios (or "P/S") of 5.6x, considering almost half the companies in China's Tech industry have P/S ratios below 2.8x. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's so lofty.

What Does Shanghai Guao Electronic Technology's P/S Mean For Shareholders?

Recent times have been quite advantageous for Shanghai Guao Electronic Technology as its revenue has been rising very briskly. It seems that many are expecting the strong revenue performance to beat most other companies over the coming period, which has increased investors' willingness to pay up for the stock. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

We don't have analyst forecasts, but you can see how recent trends are setting up the company for the future by checking out our free report on Shanghai Guao Electronic Technology's earnings, revenue and cash flow.What Are Revenue Growth Metrics Telling Us About The High P/S?

The only time you'd be truly comfortable seeing a P/S as steep as Shanghai Guao Electronic Technology's is when the company's growth is on track to outshine the industry decidedly.

The only time you'd be truly comfortable seeing a P/S as steep as Shanghai Guao Electronic Technology's is when the company's growth is on track to outshine the industry decidedly.

Retrospectively, the last year delivered an exceptional 53% gain to the company's top line. The strong recent performance means it was also able to grow revenue by 60% in total over the last three years. Therefore, it's fair to say the revenue growth recently has been superb for the company.

Comparing that to the industry, which is predicted to deliver 29% growth in the next 12 months, the company's momentum is weaker, based on recent medium-term annualised revenue results.

With this in mind, we find it worrying that Shanghai Guao Electronic Technology's P/S exceeds that of its industry peers. It seems most investors are ignoring the fairly limited recent growth rates and are hoping for a turnaround in the company's business prospects. There's a good chance existing shareholders are setting themselves up for future disappointment if the P/S falls to levels more in line with recent growth rates.

The Key Takeaway

Shanghai Guao Electronic Technology's shares may have suffered, but its P/S remains high. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

Our examination of Shanghai Guao Electronic Technology revealed its poor three-year revenue trends aren't detracting from the P/S as much as we though, given they look worse than current industry expectations. When we see slower than industry revenue growth but an elevated P/S, there's considerable risk of the share price declining, sending the P/S lower. Unless there is a significant improvement in the company's medium-term performance, it will be difficult to prevent the P/S ratio from declining to a more reasonable level.

Having said that, be aware Shanghai Guao Electronic Technology is showing 2 warning signs in our investment analysis, you should know about.

If these risks are making you reconsider your opinion on Shanghai Guao Electronic Technology, explore our interactive list of high quality stocks to get an idea of what else is out there.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.