Guangzhou Echom Sci.&Tech.Co.,Ltd's (SZSE:002420) Price Is Right But Growth Is Lacking After Shares Rocket 29%

Guangzhou Echom Sci.&Tech.Co.,Ltd's (SZSE:002420) Price Is Right But Growth Is Lacking After Shares Rocket 29%

Guangzhou Echom Sci.&Tech.Co.,Ltd (SZSE:002420) shareholders would be excited to see that the share price has had a great month, posting a 29% gain and recovering from prior weakness. Not all shareholders will be feeling jubilant, since the share price is still down a very disappointing 15% in the last twelve months.

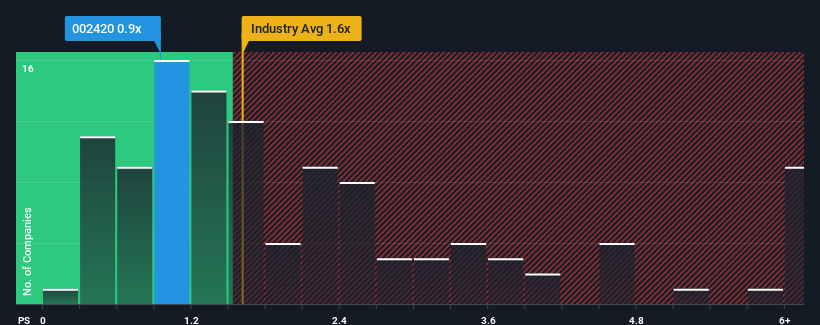

In spite of the firm bounce in price, it would still be understandable if you think Guangzhou Echom Sci.&Tech.Co.Ltd is a stock with good investment prospects with a price-to-sales ratios (or "P/S") of 0.9x, considering almost half the companies in China's Consumer Durables industry have P/S ratios above 1.6x. However, the P/S might be low for a reason and it requires further investigation to determine if it's justified.

What Does Guangzhou Echom Sci.&Tech.Co.Ltd's Recent Performance Look Like?

For example, consider that Guangzhou Echom Sci.&Tech.Co.Ltd's financial performance has been poor lately as its revenue has been in decline. It might be that many expect the disappointing revenue performance to continue or accelerate, which has repressed the P/S. However, if this doesn't eventuate then existing shareholders may be feeling optimistic about the future direction of the share price.

Although there are no analyst estimates available for Guangzhou Echom Sci.&Tech.Co.Ltd, take a look at this free data-rich visualisation to see how the company stacks up on earnings, revenue and cash flow.What Are Revenue Growth Metrics Telling Us About The Low P/S?

The only time you'd be truly comfortable seeing a P/S as low as Guangzhou Echom Sci.&Tech.Co.Ltd's is when the company's growth is on track to lag the industry.

Taking a look back first, the company's revenue growth last year wasn't something to get excited about as it posted a disappointing decline of 9.8%. The last three years don't look nice either as the company has shrunk revenue by 29% in aggregate. Therefore, it's fair to say the revenue growth recently has been undesirable for the company.

Comparing that to the industry, which is predicted to deliver 11% growth in the next 12 months, the company's downward momentum based on recent medium-term revenue results is a sobering picture.

With this information, we are not surprised that Guangzhou Echom Sci.&Tech.Co.Ltd is trading at a P/S lower than the industry. However, we think shrinking revenues are unlikely to lead to a stable P/S over the longer term, which could set up shareholders for future disappointment. There's potential for the P/S to fall to even lower levels if the company doesn't improve its top-line growth.

The Bottom Line On Guangzhou Echom Sci.&Tech.Co.Ltd's P/S

Guangzhou Echom Sci.&Tech.Co.Ltd's stock price has surged recently, but its but its P/S still remains modest. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

Our examination of Guangzhou Echom Sci.&Tech.Co.Ltd confirms that the company's shrinking revenue over the past medium-term is a key factor in its low price-to-sales ratio, given the industry is projected to grow. Right now shareholders are accepting the low P/S as they concede future revenue probably won't provide any pleasant surprises either. Given the current circumstances, it seems unlikely that the share price will experience any significant movement in either direction in the near future if recent medium-term revenue trends persist.

Before you take the next step, you should know about the 2 warning signs for Guangzhou Echom Sci.&Tech.Co.Ltd that we have uncovered.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com