Meritage Homes

MTH

Apple

AAPL

Taylor Morrison Home

TMHC

4

KB Home

KBH

5

Toll Brothers

TOL

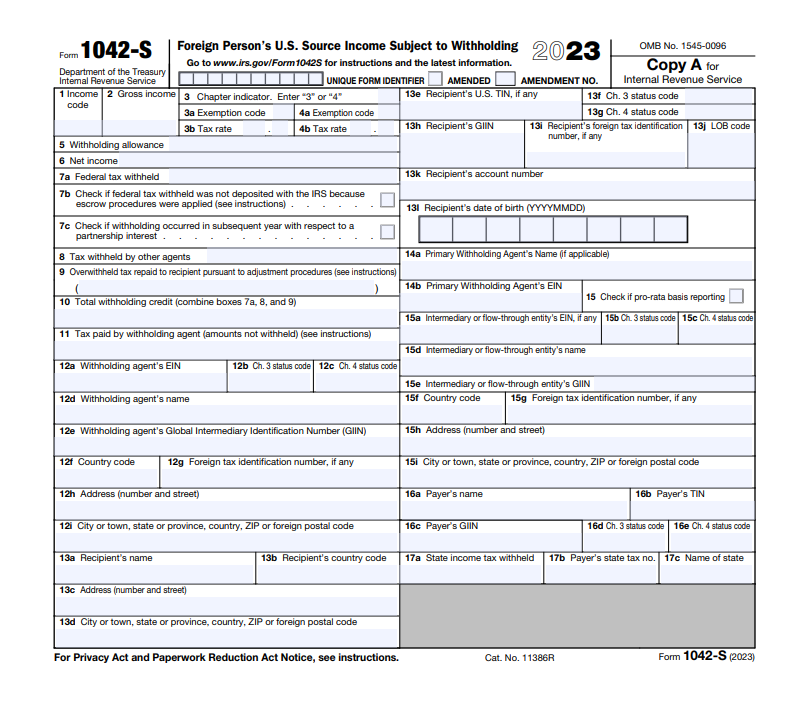

Tax Form 1042-S, Foreign Person's U.S. Source Income Subject to Withholding, is filed by withholding agent to report amounts paid to foreign persons that are described under Amounts Subject to NRA Withholding and Reporting, even if withholding is not required on the payments.

A separate Form 1042-S is required for:

● Each recipient regardless of whether or not tax was withheld

● Each type of income that was paid to the same recipient

● Each tax rate (if withholding occurred at more than one tax rate) of a specific type of income paid to the same recipient.